In the fast-paced world of business, having access to sufficient funds is essential for growth, stability, and survival. Business loans are one of the most effective ways for entrepreneurs and business owners to secure the financial resources necessary for their operations. This guide delves into the various types of business loans, their benefits, and how to navigate the application process.

What Are Business Loans?

A business loan is a financial product provided by banks, credit unions, or other financial institutions to help businesses meet their financial needs. These loans can be used for a variety of purposes, such as purchasing equipment, expanding operations, managing cash flow, or funding a new venture.

Business loans are typically repaid with interest over an agreed period, and the terms vary depending on the type of loan, the lender, and the borrower’s financial profile.

Types of Business Loans

1. Term Loans

- A lump sum borrowed for a specific purpose, repaid over a set period.

- Suitable for long-term investments like purchasing equipment, real estate, or large-scale projects.

- Can have fixed or variable interest rates.

2. Small Business Administration (SBA) Loans

- (Applicable in the U.S.)

- Government-backed loans provided through SBA-approved lenders.

- Offer favorable terms, lower interest rates, and longer repayment periods.

- Common types include the SBA 7(a) loan, SBA 504 loan, and microloans.

- Require detailed documentation and a thorough approval process.

3. Business Lines of Credit

- A revolving credit facility allowing businesses to access funds up to a set limit.

- Provides flexibility since interest is charged only on the amount used.

- Ideal for short-term funding needs, such as covering unexpected expenses or seasonal cash flow gaps.

4. Equipment Financing

- Specifically designed to purchase machinery or equipment for business operations.

- The equipment itself often serves as collateral, reducing the need for additional assets.

- Repayment terms align with the lifespan of the equipment.

5. Invoice Financing

- Also known as accounts receivable financing.

- Allows businesses to borrow money against unpaid invoices.

- Helps bridge cash flow gaps while waiting for customers to pay.

6. Merchant Cash Advances (MCAs)

- A lump sum provided in exchange for a percentage of future credit card sales.

- Offers quick access to funds but often comes with high costs and fees.

- Suitable for businesses with consistent credit card transactions.

7. Microloans

- Small loans typically provided by non-profit organizations or community lenders.

- Designed for startups or small businesses with modest funding needs.

- Maximum loan amounts vary but are generally under $50,000.

8. Commercial Real Estate Loans

- Used to purchase or renovate property for business purposes.

- Includes mortgages, construction loans, and bridge loans.

- Requires collateral in the form of the property being financed.

9. Startup Loans

- Tailored for new businesses without an established track record.

- Often require a strong business plan and personal financial guarantees.

10. Working Capital Loans

- Short-term loans to cover operational expenses, such as payroll, rent, or inventory.

- Help maintain daily operations without disrupting cash flow.

Benefits of Business Loans

Access to Capital

- Provides immediate access to funds needed for various purposes, from expansion to day-to-day operations.

Flexibility

- A wide range of loan types allows businesses to choose one that aligns with their specific needs and goals.

Preservation of Ownership

- Unlike equity financing, business loans don’t require giving up ownership stakes.

Improved Cash Flow

- Helps manage cash flow by covering gaps between expenses and revenue.

Building Business Credit

- Timely repayment of loans can enhance a business’s credit score, improving future borrowing opportunities.

Scalability

- Enables businesses to scale operations by investing in infrastructure, technology, or workforce.

Tax Benefits

- Interest paid on business loans is often tax-deductible, reducing the overall cost of borrowing.

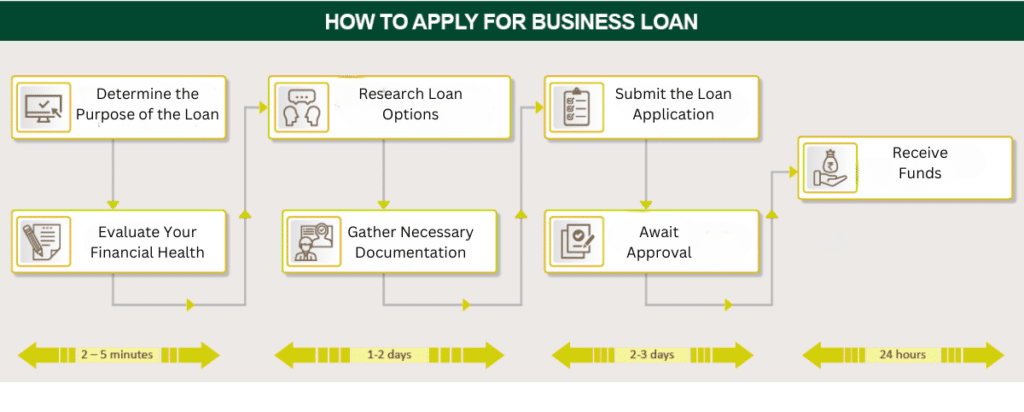

How to Apply for a Business Loan

Applying for a business loan involves several steps, and preparation is crucial to increase the likelihood of approval.

Step 1: Determine the Purpose of the Loan

- Clearly define why you need the loan. Examples include:

- Purchasing equipment.

- Expanding into new markets.

- Managing cash flow during a slow season.

Step 2: Evaluate Your Financial Health

- Review your personal and business credit scores.

- Assess your revenue, profit margins, and existing debts.

- Ensure that your financial ratios align with lender requirements.

Step 3: Research Loan Options

- Compare different lenders and loan products.

- Consider factors such as interest rates, repayment terms, and fees.

Step 4: Gather Necessary Documentation

- Typical requirements include:

- A detailed business plan.

- Personal and business tax returns.

- Financial statements (income statement, balance sheet, cash flow statement).

- Proof of collateral (if applicable).

- Legal documents, such as licenses or permits.

Step 5: Submit the Loan Application

- Complete the lender’s application form and attach all required documents.

- Be prepared to answer questions about your business and financial history.

Step 6: Await Approval

- The lender will review your application, verify information, and assess risk.

- Approval times can vary from days to weeks, depending on the loan type and lender.

Step 7: Receive Funds

- Once approved, the funds are disbursed according to the agreed terms.

Tips for a Successful Loan Application

Maintain a Strong Credit Profile

- Both personal and business credit scores impact loan approval.

- Pay bills on time and reduce outstanding debt.

Prepare a Robust Business Plan

- Demonstrate the viability and profitability of your business.

- Include projections and show how the loan will be used effectively.

Be Transparent and Thorough

- Provide complete and accurate information during the application process.

- Misrepresentation or missing documentation can delay or derail the process.

Build Relationships with Lenders

- Establishing a relationship with your bank or lender can improve your chances of approval.

Seek Professional Guidance

- Consult with financial advisors or accountants to ensure your application is strong.

Conclusion

Business loans are a powerful resource for businesses at all stages, from startups to well-established enterprises. By understanding the types, benefits, and application process, you can make informed decisions that support your business goals. Whether it’s scaling operations, managing cash flow, or investing in growth, a well-chosen business loan can be a strategic asset in achieving long-term success.

Also Read: Mortgage Loan Basics: From Application to Approval